Bittensor (TAO) Price Could Surge to $270 as Analyst Spots Adam & Eve Pattern

The post Bittensor (TAO) Price Could Surge to $270 as Analyst Spots Adam & Eve Pattern appeared first on Coinpedia Fintech News

While the broader crypto market continues to move sideways with limited momentum, Bittensor (TAO) is quietly showing signs of relative strength. The AI-focused token (TAO) has climbed around 4% in the past 24 hours and nearly 9% over the past week, standing out in an otherwise consolidating market. Now, with analyst spotting a bullish Adam & Eve pattern and derivatives data turning positive, traders are beginning to eye a potential breakout that could push TAO price toward the $270 level.

Analyst Highlights Bullish Adam & Eve Pattern

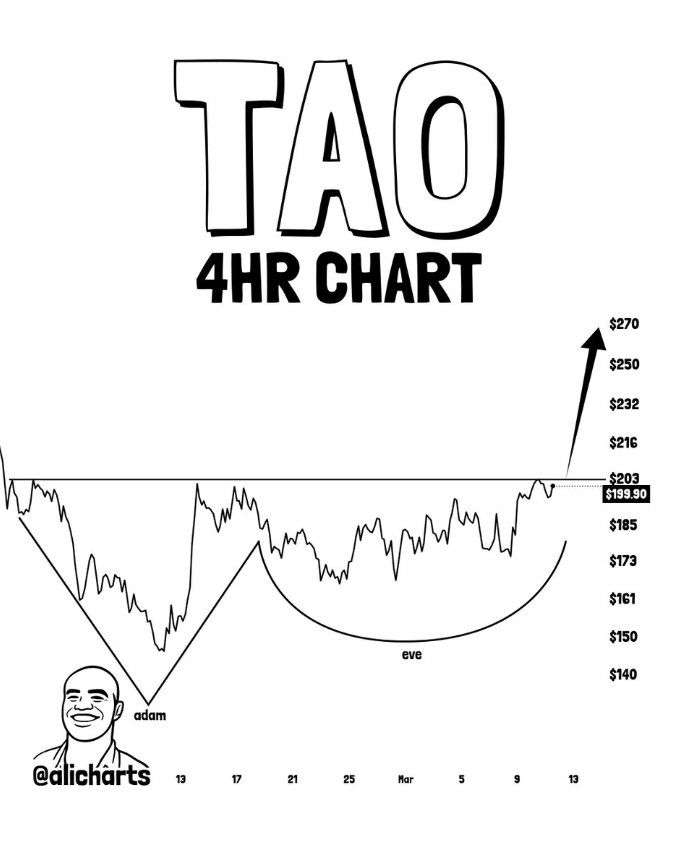

Crypto analyst Ali Martinez recently pointed out that Bittensor (TAO) appears to be forming an Adam & Eve pattern on the 4-hour chart, a technical structure that often signals the start of a strong upward move.

The pattern typically forms when a sharp “Adam” bottom is followed by a rounded “Eve” recovery, indicating that selling pressure is weakening while buyers gradually step back into the market.

If the structure confirms with a breakout above resistance, analysts suggest TAO price could rally toward the $250–$270 zone, which now stands as the next key upside target. Technical traders often view this pattern as a high-probability reversal setup, particularly when it appears alongside improving market sentiment.

Derivatives Data Signals Growing Bullish Sentiment

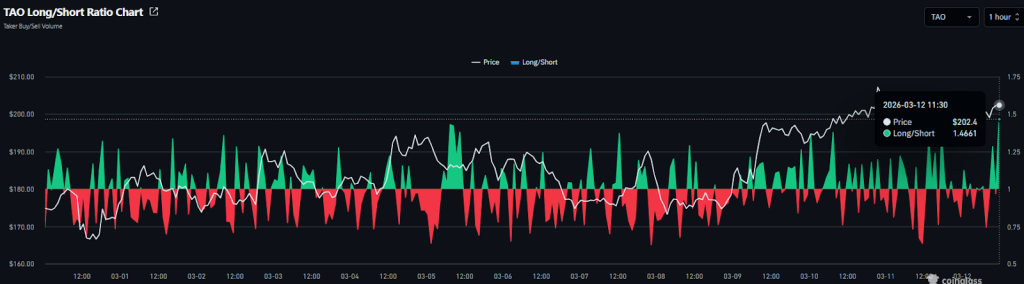

Derivatives data is also strengthening the bullish narrative around TAO price. According to Coinglass data, the TAO long/short ratio is currently hovering near 1.4, suggesting that long positions significantly outweigh short positions. A ratio above 1 generally indicates bullish trader sentiment, and the current reading shows growing confidence that TAO may continue climbing in the near term.

This shift in positioning suggests that market participants are increasingly betting on upside continuation rather than downside risk.

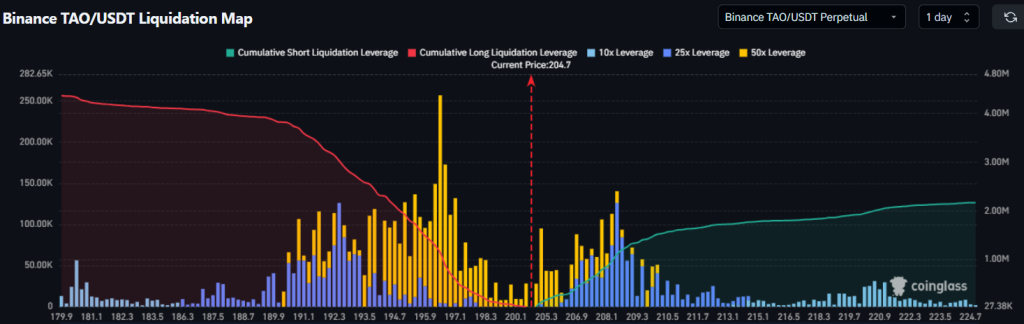

While liquidation heatmap data further highlights an interesting setup for TAO. A significant cluster of short liquidations appears above the current price zone around $205–$220. If buyers manage to push the price through this range, it could trigger forced liquidations of short positions.

Such events often lead to rapid price surge, as traders rush to close losing positions while momentum traders enter new longs. At the same time, downside liquidation clusters remain relatively limited, suggesting that current price levels continue to attract demand.

TAO Price Analysis: Is a Major Rally Next?

With technical patterns aligning, derivatives sentiment turning bullish, and price momentum strengthening, Bittensor price appears to be entering a potentially decisive phase. If TAO price manages to clear its immediate resistance zone, the next key upside targets sit near $220, followed by the $250–$270 range highlighted by analysts.

However, if the token experiences renewed volatility, TAO could retest support levels around $190–$195, where buyers have previously stepped in. For now, the token’s relative strength in a sideways market, combined with improving trader sentiment, suggests that Bittensor may be positioning for its next major move.

You May Also Like

UNI Price Prediction: Testing $4.17 Upper Band Resistance, Targets $4.50 by April 2026

Speed, Cost, and Intelligence: How Kie.ai’s Gemini 3 Flash API Balances Performance and Budget for Developers