Can I buy crypto in a retirement account? – Can I buy crypto in a retirement account?

Use this guide to compare options and to identify the primary sources you should review, such as IRS guidance and Department of Labor material, before you move assets. FinancePolice provides plain-language context and decision checkpoints but not tax or legal advice.

Short answer: can you hold crypto in a retirement account?

Yes, but with important limits and differences by account type: some tax-advantaged accounts allow direct crypto holdings while many employer 401(k) plans do not. The IRS treats cryptocurrency as property for tax purposes, which affects how transactions inside and around retirement accounts are reported IRS virtual currencies.

Compare account types and custodian support for crypto

Use as a simple self-check before you proceed

In short, a crypto retirement account is possible mainly through a self-directed IRA that uses a qualified digital-asset custodian, or indirectly through funds or securities that give crypto exposure. Read the sections below to review custody, tax, and regulatory issues before making a move.

What a crypto retirement account means: account types and basic options

Tax-advantaged account types overview

When people talk about a crypto retirement account they usually mean a tax-advantaged account, such as a traditional IRA, Roth IRA, or an employer 401(k). A self-directed IRA is a variation that gives the owner broader asset choices and can permit assets beyond typical mutual funds and stocks.

Availability is not set by a single law that forbids crypto in retirement accounts; it depends on whether your custodian and account arrangement permit those assets, and whether a plan sponsor includes crypto-linked options on a 401(k) menu. For practical descriptions and how providers commonly handle this, see a consumer guide to holding crypto in retirement accounts How to Hold Cryptocurrency in an IRA or 401(k) and an explainer from SoFi.

Two basic routes: direct crypto holdings vs. crypto-linked funds

There are two common ways to get crypto exposure for retirement saving. One route is direct ownership of tokens inside a self-directed IRA that uses a digital-asset custodian. The other is gaining exposure through a fund, trust, or other security that tracks crypto, which a more conventional account may allow without holding tokens directly.

Direct ownership requires custody that can secure keys and satisfy retirement-account rules, while funds behave more like traditional securities and often avoid the custody and key-management issues that come with tokens.

In short, a crypto retirement account is possible mainly through a self-directed IRA that uses a qualified digital-asset custodian, or indirectly through funds or securities that give crypto exposure. Read the sections below to review custody, tax, and regulatory issues before making a move.

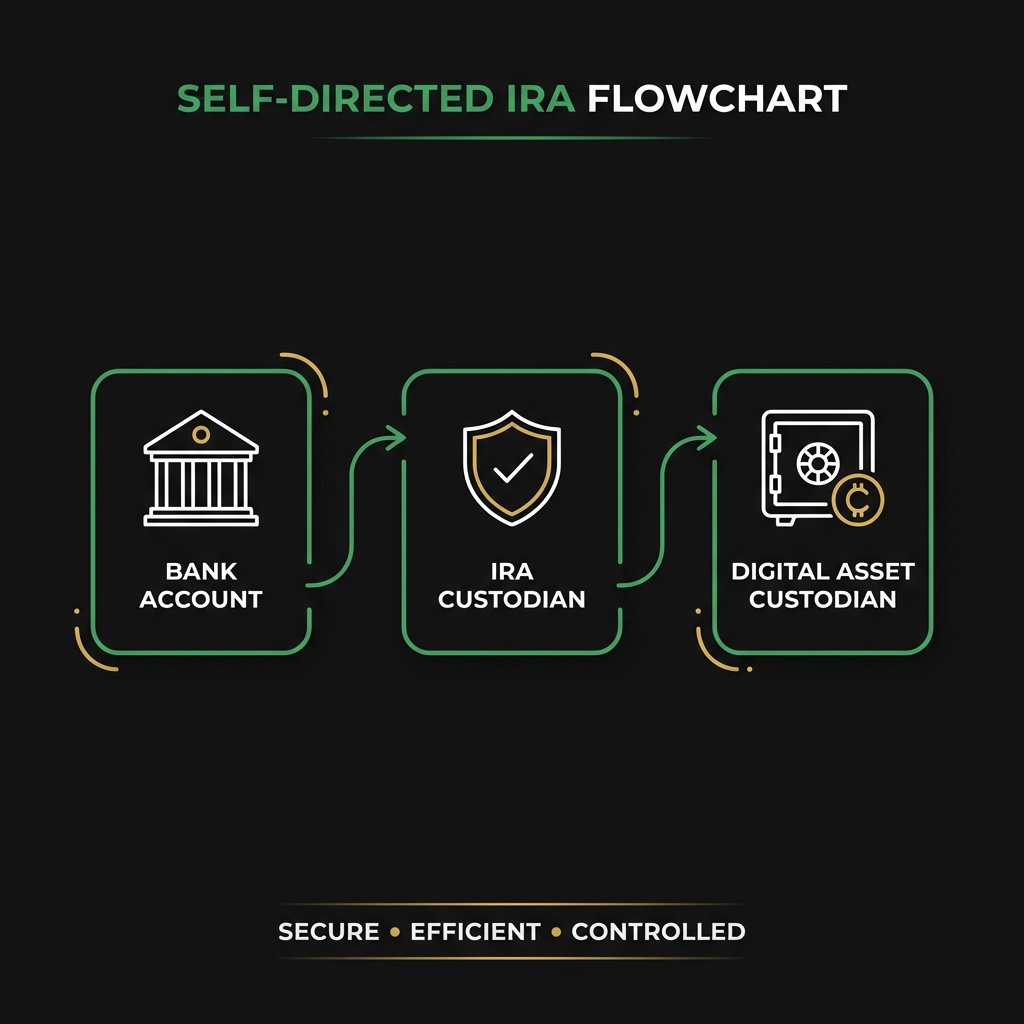

How self-directed IRAs let you buy and hold crypto

What a self-directed IRA is

A self-directed IRA is an IRA that permits a wider range of investments than a standard broker IRA, often including real estate, private placements, and in many cases direct digital assets. Many readers who want to buy crypto for retirement turn to a self-directed IRA because it is the most common path to direct token ownership.

Self-directed IRAs commonly require a custodian or trustee to hold the account and to follow IRA rules; when crypto is involved, a separate qualified digital-asset custodian typically holds the keys or token custody services. See guidance from providers such as Directed IRA when comparing custody models.

In many cases you can buy cryptocurrency inside a retirement account, but it depends on the account type and custodian; direct ownership is most common in self-directed IRAs using qualified digital-asset custodians, while employer 401(k) plans rarely offer direct token options.

If you use a self-directed IRA, expect a multi-step process: choose a compatible provider, open the account with the IRA custodian, fund or transfer assets into the account, and then instruct the custodian to purchase or accept the crypto. Providers and exact steps differ, so compare processes, timelines, and fees carefully.

Typical custody and provider models

Most self-directed IRA models separate the IRA custodian from the digital-asset custodian: the IRA custodian handles the retirement account administration while a third-party digital custodian holds private keys and manages blockchain-level custody. This split is common and intended to align retirement-account controls with secure crypto custody practices.

Provider models vary. Some firms offer an integrated experience that coordinates account opening, transfers, and trading, while others require more manual steps and separate contracts with a digital custodian. Fees and service models differ accordingly, and some custodians only support certain token types or custody arrangements.

Why direct crypto in employer 401(k) plans is uncommon

Provider menus and plan fiduciary considerations

Standard employer 401(k) menus rarely include direct crypto holdings as an investment option, and availability varies by administrator and plan sponsor. That limited availability is often a product decision rather than a categorical legal ban.

Part of the reason is fiduciary caution. Department of Labor guidance and related regulator commentary have repeatedly urged plan fiduciaries to be careful before adding digital assets to ERISA plan lineups, citing custody, valuation, liquidity, and fraud concerns Guidance for ERISA Plan Fiduciaries on Digital Assets.

Alternatives for plan participants

If your 401(k) plan does not offer direct crypto you still have options. One approach is to use a self-directed IRA outside the employer plan for direct ownership. Another is to look for crypto-linked funds or securities that may be available on the plan menu, or to buy crypto in a taxable account while continuing to use retirement accounts for other long-term holdings.

Choosing between these depends on your time horizon, tax strategy, and how much of your retirement portfolio you want in higher-volatility assets.

Custody and choosing a qualified digital-asset custodian

Why custody matters for retirement accounts

Custody for crypto is different than custody for cash or listed securities because tokens require key management and secure storage. For retirement accounts the stakes can be higher because poor custody or a lost key can create an irrevocable loss inside an account that was meant to provide long-term benefits.

Regulators and advisors often point to custody, insurance arrangements, and clear segregation of client assets as core concerns when a retirement account holds crypto. Choose a custodian that documents how client assets are segregated and what insurance or recovery processes are in place.

Check custodian security and reporting before you move assets

Check the selection checklist below to compare how a potential custodian secures keys, segregates assets, and reports valuations before you move funds into an account.

Learn how FinancePolice works with advertisers

What to look for in a custodian

When evaluating a digital-asset custodian for a retirement account, consider these practical criteria: regulatory standing, segregation of client assets, multi-party key management or cold storage practices, insurance coverage, transparent fee schedules, and reporting capabilities for tax and retirement-account compliance.

Many self-directed IRA arrangements use a trustee plus a third-party digital custodian, so verify which party performs each function and ask how transfers, custody fees, and statement reporting work together.

Tax basics: how the IRS treats crypto in retirement accounts

IRS classification of crypto

The IRS classifies cryptocurrency as property rather than currency, which affects how gains and dispositions are taxed when they occur outside of a retirement account, and how movements around tax-advantaged accounts should be documented IRS virtual currencies.

Within a properly maintained retirement account, trades and sales generally do not create immediate taxable events for the account holder, but transfers, rollovers, or otherwise mishandled transactions can produce tax consequences if rules are not followed precisely.

Common tax traps and reporting points

Key tax concerns include documenting cost basis and fair market value when assets move between accounts or when distributions are taken. If assets are removed improperly or if a prohibited transaction occurs, taxable distribution rules can apply, and penalties or tax charges may result.

For retirement accounts holding crypto, keep detailed records of transfers, timestamps, and valuations and consult the IRS guidance or a tax professional for complex moves to avoid unintended tax outcomes.

Regulatory and fiduciary warnings to be aware of

DOL and SEC guidance summarized

Federal regulators have issued warnings and guidance that plan fiduciaries should consider carefully before adding digital assets to retirement plan menus or account options, noting real risks in custody, valuation, liquidity, and recordkeeping Guidance for ERISA Plan Fiduciaries on Digital Assets. Read more in our crypto coverage.

SEC investor alerts have also highlighted investor-facing risks such as fraud, market manipulation, and the evolving classification of tokens, so remain aware that enforcement and guidance can change over time.

Open regulatory questions

Policy and regulatory work around token classification and custody responsibilities continue to evolve, and possible future rulemaking or enforcement changes could affect how retirement plans and custodians treat crypto. Verify the latest guidance before changing plan lineups or account types.

Step-by-step: how to set up and fund a self-directed IRA for crypto

Open and verify the account

Step 1 is to choose a self-directed IRA custodian that supports digital assets and to open the account. Confirm which tokens the custodian will accept and what identity and verification steps are required. See a provider guide such as AltoIRA’s guide when comparing onboarding steps.

Step 2 is to decide whether you will fund by new contributions or by a rollover or transfer from another retirement account. Rollovers often require careful timing and documentation to avoid taxable distributions.

Fund by contribution or rollover

If you roll over funds from an existing retirement account, follow the custodian s rollover instructions exactly and retain transfer receipts. If you make a new contribution to the IRA, observe contribution limits and reporting rules for traditional and Roth IRAs.

After funds arrive in the self-directed IRA, instruct the custodian or the connected digital-asset custodian to purchase the specified crypto or to accept a token transfer, and document the trade confirmations and custody receipts.

Direct purchase and recordkeeping

Recordkeeping is essential: save transaction confirmations, custodian statements, transfer receipts, and any fair market value calculations used for periodic reporting. These documents can be important for tax and compliance verification later.

Allow extra time for operational steps, since some custodians have processing windows or require settlement steps that can delay execution and affect the price at which a trade occurs.

Valuation, recordkeeping, and reporting best practices

How to value crypto in retirement accounts

Valuation for crypto often uses a consistent market data source and timestamps. Pick a reliable exchange or index that your custodian accepts for fair market value and use consistent methods across reporting periods to avoid discrepancies.

Because price can move quickly, include timestamps and the source used for each valuation, and keep a copy of the trade confirmation that shows price and quantity for each transaction.

Recordkeeping checklist

Essential records include transaction history, custodian statements, transfer receipts, trade confirmations, and any correspondence that documents how assets were valued or moved between accounts. Retain these in case of tax or plan-administration questions.

Poor recordkeeping can create compliance headaches and potential tax issues, so err on the side of thorough documentation and save records in multiple secure places.

Fees, liquidity, and cost trade-offs to consider

Typical fee types

Fees can include custody fees, transaction fees, account administration fees, and third-party custodian charges. Compare the total cost of holding crypto inside a retirement account with alternatives such as holding crypto in a taxable account or using a crypto-related fund.

Higher custody or administration fees can erode returns over time, and some custodians charge additional fees for transfers, monthly statements, or special services like token recovery attempts.

Liquidity and execution issues

Execution timing matters: some retirement-account custody arrangements introduce delays that make it harder to sell quickly. If immediate liquidity is important to you, confirm a custodian s typical execution timelines and any restrictions on withdrawals or sales.

Consider whether the liquidity trade-offs inside a retirement account align with your time horizon and whether holding certain crypto within long-term retirement savings is appropriate for your risk tolerance. For broader investing context see our investing category.

Real scenarios and examples: rollovers, direct purchases, and fund alternatives

Example 1: rollover to a self-directed IRA

Scenario: An investor wants direct token ownership. They open a self-directed IRA, initiate a trustee-to-trustee rollover from an existing IRA, and then instruct the custodian to purchase tokens through the connected digital-asset custodian. Timing and documentation are critical to avoid unintended taxable events.

Operationally, the investor should confirm the token list the custodian accepts, watch for processing windows, and save all transfer receipts and trade confirmations for future reference.

Example 2: buying crypto in a taxable account while saving in retirement accounts

Scenario: An investor prefers to keep retirement accounts in broadly diversified holdings and uses a taxable brokerage to buy crypto directly. This approach separates speculative or high-volatility positions from core retirement savings and may simplify tax reporting for retirement accounts.

This path can be sensible if you want immediate trading flexibility while preserving retirement accounts for long-term, tax-advantaged growth strategies.

Example 3: using crypto-linked funds if available on a plan menu

Scenario: A 401(k) plan offers a crypto-linked fund. The investor gains exposure without direct token custody, and the investment behaves more like other funds in the plan. This avoids some custody and key-management concerns but still exposes an investor to price volatility and fund fees.

When a plan menu includes a crypto-linked option, confirm the fund s structure, fees, and how it sources its underlying exposure before allocating a meaningful share of retirement savings to it.

Common mistakes and compliance pitfalls to avoid

Operational errors that trigger taxes

Frequent mistakes include improper rollovers or transfers, moving tokens into a personal wallet that is not held by the custodian, and missing documentation that shows an asset remained in the retirement account. Such errors can be treated as taxable distributions.

To avoid these outcomes, follow custodian instructions precisely, keep transfer receipts, and confirm that the digital-asset custodian accepts and documents token custody for the IRA.

Security and custody errors

Using a nonqualified wallet or sharing private keys can create irreversible loss. For retirement accounts, use custodial arrangements that meet the account s documentation and custody requirements and avoid attempting to hold private keys outside approved custodian workflows.

If you are unsure about a procedure, stop and verify with the IRA custodian before moving tokens or keys between accounts.

A decision checklist: is holding crypto in your retirement account right for you?

Questions to ask your custodian

Ask whether the custodian supports the tokens you want, how assets are segregated, what fees apply, how valuations are reported, and what documentation you will receive. Confirm processing times for purchases and transfers and whether the custodian has experience with retirement accounts.

Also ask about insurance coverage, recovery procedures for lost keys, and how the custodian handles corporate actions or forks, if applicable.

Personal factors to weigh

Consider your risk tolerance, time horizon, diversification needs, and whether you are comfortable with the custody and recordkeeping responsibilities that come with direct token ownership. Compare the total costs and the liquidity trade-offs with alternatives before proceeding.

When in doubt, verify custodian policies, review IRS and DOL guidance, and consult a tax professional for complex moves.

Conclusion and practical next steps

Crypto can be held in retirement accounts in specific setups, most often through self-directed IRAs that use qualified digital-asset custodians, or indirectly through crypto-linked funds where available. Holding tokens in a retirement account requires careful attention to custody, fees, and tax documentation.

Next steps: check whether your custodian supports crypto and what fees and custody arrangements they require, read IRS guidance on virtual currencies and DOL guidance for fiduciaries, and consider professional advice when planning rollovers or complex transfers. For recent market context see our recent bitcoin analysis.

Often yes in a self-directed IRA if the custodian accepts those tokens, but availability varies by custodian and account setup and you should confirm supported tokens and custody procedures first.

Trades inside a properly maintained tax-advantaged account typically do not create immediate taxable events, but transfers or prohibited transactions can have tax consequences, so keep careful records and verify rules with a tax professional.

A taxable account can offer faster trading and simpler custody, which some investors prefer for high-volatility assets; choosing depends on your horizon, tax situation, and willingness to manage custody and recordkeeping.

If you decide to proceed, use the checklist in this article to compare custodians and review operational steps before initiating rollovers or purchases.

References

- https://www.irs.gov/individuals/virtual-currencies

- https://www.nerdwallet.com/article/investing/crypto-in-ira-401k

- https://www.dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-center/publications/cryptocurrency-and-erisa-guidance

- https://financepolice.com/advertise/

- https://www.sofi.com/learn/content/how-to-hold-crypto-in-an-ira/

- https://directedira.com/cryptocurrency-and-precious-metals-in-your-retirement-account/

- https://www.altoira.com/insights/buy-crypto-in-ira-a-guide-for-individual-investors

- https://financepolice.com/category/crypto/

- https://financepolice.com/bitcoin-price-analysis-btc-reclaims-92000-as-market-awaits-fed-decision/

- https://financepolice.com/category/investing/

You May Also Like

In ‘Running With Scissors,’ Cavetown learns to accept that risk is in everything

EUR/CHF slides as Euro struggles post-inflation data