MicroStrategy’s Saylor Signals Imminent Bitcoin Buy Amid MSTR Stock YTD Decline

Michael Saylor is signaling another aggressive Bitcoin accumulation for Strategy (formerly MicroStrategy).

This signals that the firm is down on its high-stakes treasury strategy even as its MSTR stock falters.

Why Saylor is Teasing a New Bitcoin Buy for Strategy

On December 21, Saylor posted a cryptic image to X captioned “Green Dots ₿eget Orange Dots,” referencing the company’s “SaylorTracker” portfolio visualization.

The post continues a year-long pattern Saylor has used to hint at a new BTC purchase. Notably, such a weekend teaser is usually followed by a Monday morning SEC filing confirming a significant acquisition.

Meanwhile, a new purchase would add to an already staggering hoard.

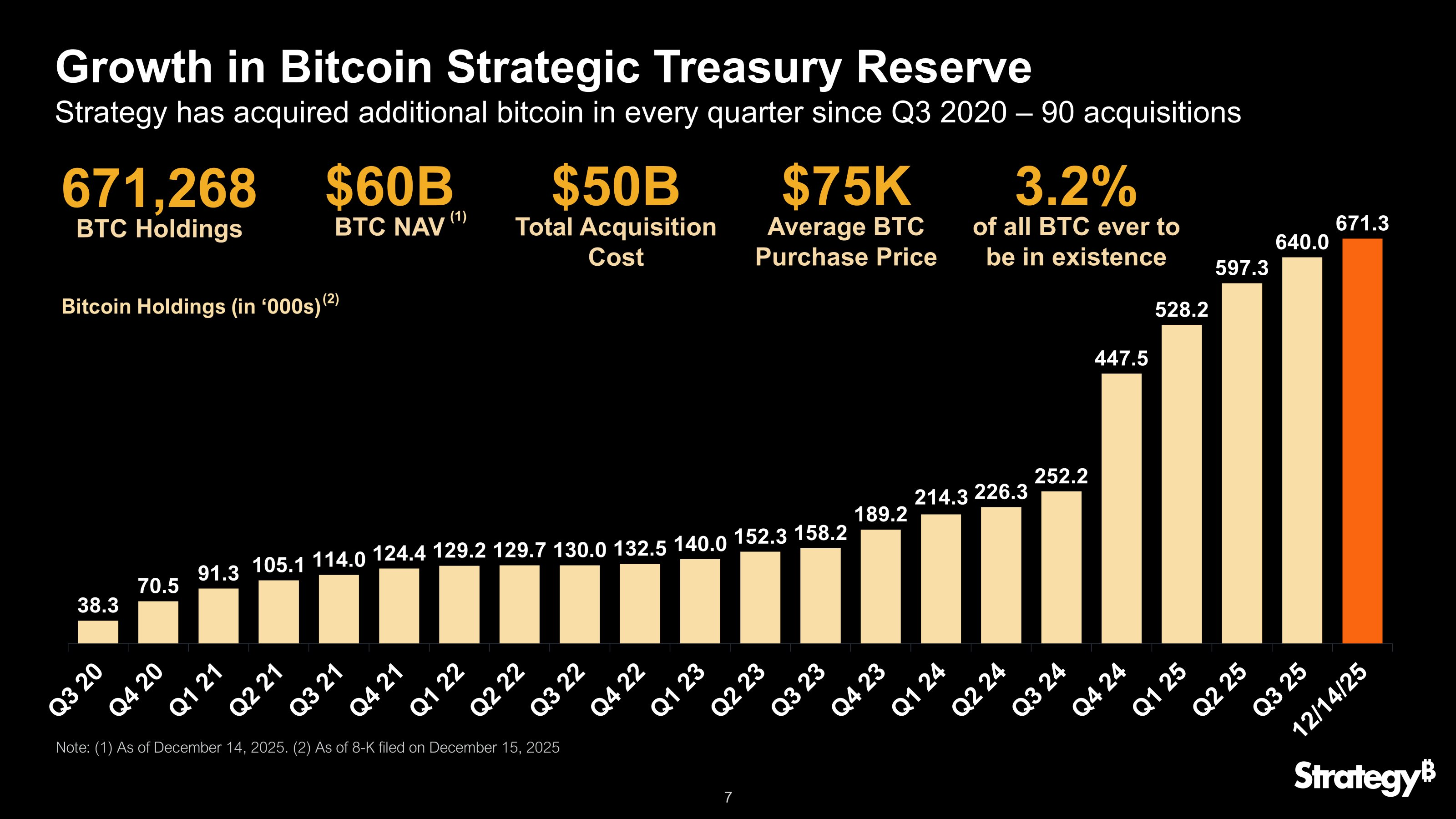

As of press time, Strategy held 671,268 BTC—valued at roughly $50.3 billion—representing 3.2% of the total Bitcoin supply.

Strategy’s Bitcoin Holdings. Source: Strategy

Strategy’s Bitcoin Holdings. Source: Strategy

However, the market has punished the stock in 2025. MSTR shares have collapsed 43% year-to-date to trade around $165, mirroring Bitcoin’s 30% retreat from its October peak of $126,000.

While the company touts a “BTC Yield” of 24.9%—a proprietary metric measuring the accretion of Bitcoin per share—institutional investors are increasingly focused on the looming external risks rather than internal yield metrics.

However, the most immediate threat to Saylor’s strategy is not Bitcoin’s price, but a potential regulatory reclassification.

MSCI is considering removing Strategy Inc. from its global indices during its February review. The index provider has flagged concerns that the firm now functions more like an investment vehicle than an operating company.

Market analysts have pointed out that the financial implications of such a move are severe.

JPMorgan estimates that an exclusion would trigger approximately $11.6 billion in forced selling as passive ETFs and index-tracking funds liquidate their MSTR positions.

This mechanical selling pressure could decouple the stock from its Bitcoin holdings, creating a liquidity spiral.

In response, Strategy has launched a vigorous defense.

The firm called the MSCI proposal “arbitrary, discriminatory, and unworkable,” arguing that it unfairly targets digital asset companies while ignoring other holding-heavy conglomerates.

So, Saylor’s potential new purchase serves a dual purpose: it lowers the company’s average cost basis during a market correction, but more importantly, it signals to the market that despite the MSCI threat and the stock’s poor performance, the “all-in” strategy remains unchanged.

You May Also Like

What We Know So Far About Reported Tensions at Bitmain

Galaxy Digital’s head of research explains why bitcoin’s outlook is so uncertain in 2026

Copy linkX (Twitter)LinkedInFacebookEmail