Bitcoin under pressure as yields rise, Iran conflict, inflation risk

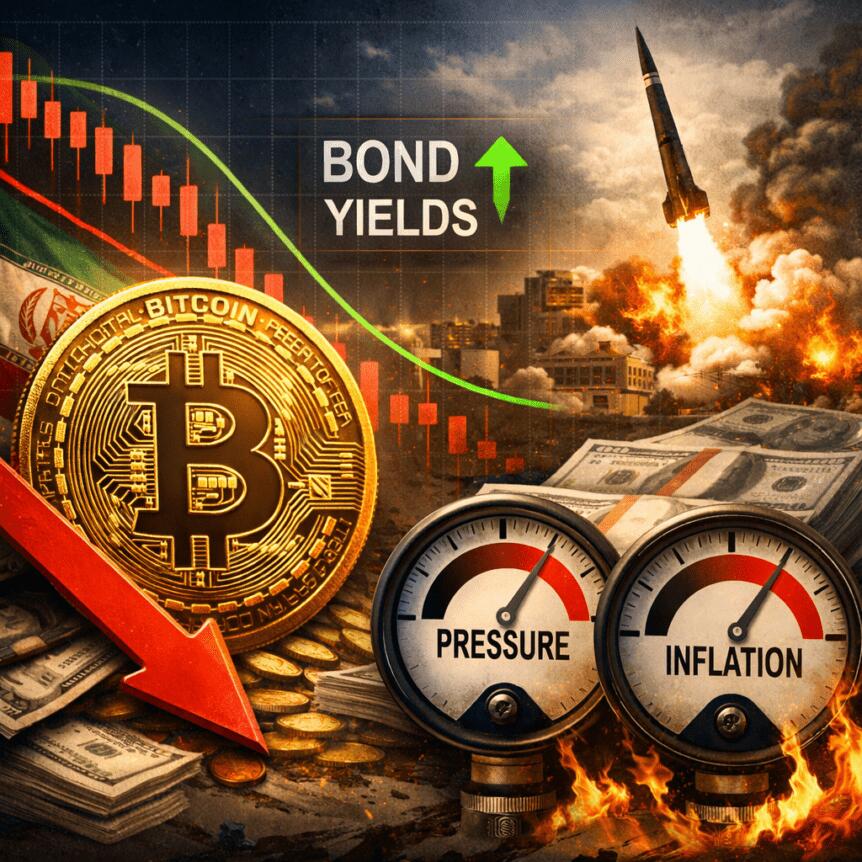

A risk-off mood swept across crypto and traditional markets as geopolitical tensions and stubborn inflation kept investors cautious. Bitcoin tested the $67,500 support level on Monday as traders paused after a run higher, while gold endured a sharp pullback described as one of its steepest corrections in more than five decades. Oil extended its rally, trading above the $90 per barrel threshold on renewed concerns about conflicts in the Middle East, heightening inflation pressures even as markets gauged the trajectory of U.S. monetary policy.

In parallel, U.S. Treasuries came under selling pressure, with the 5-year yield surging to around 4.10% — a nine-month high — as investors demanded better returns in a uncertain macro backdrop. The S&P 500 also slipped to its weakest level in more than six months, underscoring a broad shift toward liquidity. Market data pointed to a meaningful shift in rate expectations, with the probability of a July rate hike climbing to roughly 20% according to the CME FedWatch tool, signaling a tighter policy stance ahead.

Key takeaways

-

Bitcoin tested the $67,500 support as risk assets sold off alongside a sharp gold correction and a surge in oil prices driven by geopolitical fears.

-

U.S. 5-year Treasury yields rose to about 4.10%, a nine-month high, as markets price a higher likelihood of further rate hikes this year (roughly 20% probability for a July move).

-

Oil breached the $90 level on Middle East tensions, intensifying inflationary pressures at a moment when investors reassess policy and growth risks.

-

Debt risk and tech stock softness added to the cautious tone: the U.S. national debt topped $39 trillion, while major tech names faced meaningful drawdowns on several fronts, including AI-euphoria and growth concerns.

Markets in risk-off mode amid macro and geopolitical shocks

Bitcoin’s move to test the key $67,500 support zone reflected a market attempt to balance recovering sentiment with renewed caution. The rapid correction in gold prices—described by some as the sharpest in more than five decades—illustrates how investors pivoted toward cash and short-duration assets as inflationary pressures persisted and the path of U.S. monetary policy remained uncertain. Oil’s ascent above $90 a barrel added another layer of complexity, feeding concerns about higher consumer costs and potential policy responses crafted to contain inflationary spillovers.

Geopolitical developments surrounding Iran dominated the narrative in trade desks and policy circles. Market observers noted that oil’s rally would likely keep inflation prints under scrutiny and complicate the Federal Reserve’s task of calibrating policy to slow growth without tipping the economy into recession. The Washington Post highlighted broader debates over military posture and cost, reporting that U.S. authorities debated options including a potential deployment of additional troops in the region to counter Iran’s influence around critical chokepoints. While these reports underscored escalation risk, traders stressed that policy clarity and inflation data would ultimately guide near-term price action for risk assets, including Bitcoin.

From a pure market-structure perspective, the risk-off tilt was reinforced by a retreat in equities. The S&P 500’s dip toward multi-month lows signaled that investors were de-risking amid uncertainty over how elevated energy prices, geopolitical tensions, and slower growth might interact with corporate earnings. On the rate front, the implied path of policy tightening appeared to broaden: the CME FedWatch Tool showed a meaningful probability that the Federal Reserve could raise rates by July, albeit with a still-contingent trajectory depending on incoming data on inflation and the labor market.

Policy trajectory, debt dynamics, and the tech earnings backdrop

Beyond the immediate geopolitical chatter, traders weighed the longer arc of monetary policy. The combination of higher yields and persistent inflation expectations has kept a lid on risk assets, with many market participants reassessing whether a soft landing remains plausible in a climate of elevated funding costs and debt issuance. In this environment, Treasuries faced continued selling pressure as investors demanded higher yields to compensate for ongoing macro headwinds.

Meanwhile, the broader debt landscape remains a talking point for investors concerned about fiscal sustainability. U.S. government debt has surpassed $39 trillion, highlighting the fragility of the macro backdrop where wage growth and consumer prices interact with fiscal stimulus and military spending. This backdrop has intensified debates about the pace of further monetary tightening and the risk of policy missteps that could weigh on asset prices, including Bitcoin, which despite resilient on-chain metrics, has to contend with a macro regime that favors liquidity preservation during stress periods.

In the tech ecosystem, the mood pivoted as investors evaluated the sustainability of AI market strength versus the fundamentals of a broad-based rally. Reuters reported that OpenAI, the creator of ChatGPT, was courting private-equity investors with a guaranteed minimum return of 17.5% even as broader profitability remained challenged. The dynamic underscored the tension between AI enthusiasm and the need for disciplined capital deployment in a high-rate, high-cost funding environment. The sector-wide pullback in tech stocks—names like Google, Meta, and IBM registering material declines over the past several weeks—further reflected the recalibration away from speculative momentum toward more cautious allocations.

From a practical standpoint, the pullback did not erase the undercurrents of crypto-specific demand signals observed in on-chain activity and institutional interest. Some metrics suggested that Bitcoin remained resilient on a structural basis even as price action traded within a broad range. However, the combination of rising yields, fragile risk sentiment, and systemic debt growth kept upside momentum in check and kept the door open for further volatility as new data prints and policy cues arrive.

For investors, the message is nuanced. While the macro risk-off environment tends to weigh on risk assets, Bitcoin’s role as a diversifying, non-sovereign store of value remains a focal point for portfolios seeking hedges against fiat instability. Yet the narrative remains highly conditional on inflation trajectories and the policy response to geopolitical shocks. The divergences between on-chain indicators and macro price action suggest a period where crypto markets could outperform in certain risk-off scenarios while still grappling with broader macro headwinds in others.

What to watch next

Looking ahead, traders will be closely watching inflation data, labor market signals, and the pace of energy prices to gauge how much further the Fed might tighten and when. Any escalation in Iran-related tensions or shifts in Middle East risk could renew a bid for safer assets and recalibrate expectations for both traditional markets and crypto equities. On the policy side, the next round of statements and minutes from the Fed, alongside real-time economic indicators, will shape the probability curve for rate moves and help determine whether BTC and other digital assets can sustain a constructive breakout or drift into a renewed risk-off regime.

This article draws on market readings and reporting from Cointelegraph, The Washington Post, Reuters, and related outlets to outline the evolving risk landscape. As always, readers should conduct their own research and consider how macro forces, geopolitical developments, and sector-specific dynamics interact in shaping crypto markets.

This article was originally published as Bitcoin under pressure as yields rise, Iran conflict, inflation risk on Crypto Breaking News – your trusted source for crypto news, Bitcoin news, and blockchain updates.

You May Also Like

XRP Price Prediction: Targets $1.50-$1.60 by April 2026 Amid Technical Consolidation

Solana Price Prediction: Weekly Support Still Intact